A use case study

I’m a small time investor in cryptocurrencies. Really small. I kicked myself enough for the times I could have bought Bitcoin at $40 or Ethereum at $7, but didn’t.

While if I had done so I’d have signed my lottery ticket already, I’ve never been more excited by the prospect of the future of Regular Guy finance than I am right now.

While Bitcoin and ETH are sucking up the media attention, the Terra project has been quietly revolutionizing what it means to buy things and save money for normal people.

You already use digital cash

Real cash is annoying. I’ve got an ancient coin jar. A few dollars make my wallet difficult to get out at the drive-through—and I’m what my adult kids call ‘old’.

What I really do is pay for my daily purchases with a credit card, pay that off every month with online bill pay, and count bonus miles. I never see any of those dimes. I’m not sure they really exist except on a balance sheet as a number.

What makes this functional is the settlement layer: currently an anachronistic set of agreements and archaic interbank payment systems that require a lot of personnel, hardware and facilities to operate—and days to complete. If you’re familiar with the experience of trying to cash a personal check for the full amount, and being told “you can deposit and withdraw it in 3 days”, that’s why. Bank 1 has to contact Bank 2 and verify the required funds are there, then they have to agree on a cash transfer and associated costs, and pay their CEOs millions to manage the process.

Your cash is not your own

The term in the Crypto community is ‘custodial’. You are trusting someone else to handle your money for you. You’re trusting that the bank balance sheets are accurate, and they won’t drain or freeze your funds, that they’ve sufficiently vetted their employees. You’re trusting there’s enough deposited on their balance sheets for you to be able to use your funds when you want to.

You ask them for permission to access your funds. There are strict limits on these permissions and trusts, and your ability to use your funds is limited to the scope of the institutions. This is in order to keep the system of trusts working; if the trusts broke down, chaos ensues.

What if this were not the case? What if, instead of a number on a database, your cash actually belonged to you, and you could access and use it directly with an unbreakable algorithmic settlement layer in seconds, with zero third-party permissions required? We call that ‘non-custodial’: you hold the keys to your funds and only you can access them.

Riches at the edge of the balance sheet

Banks make their money renting your cash for interest on car and house payments— this won’t be a surprise. However, what you may be less aware of is the profits to be made at the edge of the balance sheet—the user-to-user transactions that get your coffee and lunch in your hand, that you’re using the bank’s virtual cash to pay for.

This is called a ‘payment gateway’, and Clover, Square, Paypal, Stripe, Visa, Mastercard and America Express are names you may be familiar with that operate in this space.

If you are an average consumer, you’re not aware of the costs of the payment gateway, as the fees are generally hidden within the cost of the item. However, if you are a vendor, you’re keenly aware of the 2-3% costs on every transaction. For a small shop, $5000 in daily turnover results in $100-150 in additional costs. Some small vendors have a minimum purchase for credit use to help defray the expense. Others have different pricing to incentivize physical cash, particularly gas stations.

This is the cost of an anachronistic settlement layer. The profits of the payment gateways as they gatekeep these trusts are huge: Visa alone makes $20 billion a year in net profit. To me that looks like inefficiency.

An alternative path

If ‘digital cash’ was truly immutable and digital, and the settlement layer was made up of unbreakable algorithms that operate with maximum efficiency, anchored by a team of globally distributed validators who have individually risked their capital to maintain this network at the risk of being slashed from the network and excluded if they try to mess with it or fail to maintain it properly, with changes to the algorithms governed by votes by millions of fellow small investors like myself, you’d arrive at the architecture of the Terra Network.

I won’t go into the technical details, which are plentiful (see https://docs.terra.money); I’ll stick with the big picture for now.

As a small-time ‘staker’ in the Terra network, I see a small-time return on the value of my stake. A payment using the Terra network costs $.001 or so, and that profit goes to the stakers on the network. In my Terra Station app, I can watch the real-world adoption of Terra rise and spread. I’ve got 500 South Korean Won in there right now, representing a slice of the $1.8 million in KRW that is settled by the network on a daily basis. I’ve also got .000467 Thai Baht—but that coin was introduced to the system only this month. Tiny fractions of value to be sure, but adoption is still very early, and low fees will result in fractional amounts.

What I’ve also seen grow is both the value of and the return on the Luna token that stabilizes and mobilizes the settlement layer for the national currency proxy coins in Terra. From ~15% return 2 months ago, to ~40% today, this is a fluctuating number that generates the profit for those who are holding the network token and holding the network itself accountable. These increases represent the volume and momentum of the payments system adoption shifting to the upside, which has been on a tear recently.

Breaking new ground in options

What else all this means for normal consumers who are not crypto fanatics and never will be, is that applications and application integrations are now in development to make the truly digital dollar usable in new ways for everyday people who want and need to know nothing about settlement layers, crypto and finance.

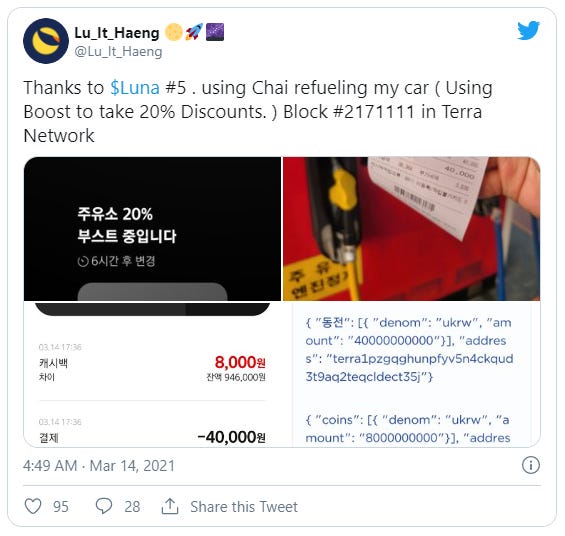

To see what that looks like, see happy user @Lu_It_Haeng’s jubilant twitter posts. Looks just like Venmo or Zelle.

Where it’s different is that with such low costs and payments being managed algorithmically, new options emerge. Here are 2: currently one is in operation, the other is in proposal.

Anchor: https://anchorprotocol.com

Anchor is a fully-functional savings protocol that leverages staking profits and returns them in savings yield on a continuously-compounding basis for depositors—at a rate of 20%. For me this currently means ~$.50/day in profit. Funds are not locked for any period and are non-custodial, so I have 100% control over my funds, subject to the terms of the algorithms. Good luck getting anything close to that from your bank.

Loans are also instantly available, but right now must be collateralized at a max rate of 50% by staked Luna. More options will follow. I’m looking forward to the possibility of a digitized car loan anchored by a digital car deed, governed by a smart contract, transactable in seconds from the shop floor.

20% profit on bill pay funds:

The high profit of Anchor-deposited funds, combined with the possibility of embedding access to Anchor with 7 lines of code, makes 20% daily profit on cash you have to spend monthly possible.

Think about this: how much money do you turn over in expenses per month, paying your utilities, car loans and mortgage? How often do you get paid on the day those bills are due? How much is your bank paying you for holding onto your cash for the 15 days or whatever from when you get paid to when the vendor needs the payment? I calculate somewhere in the region of $3-6 dollars a day could be earned by putting my personal bill payment cash in Anchor and paying the bill 1 or 2 days early. Chump change adds up.

Banks ingeniously offer free online bill-pay. But they are surely using your cash for their profit while your capital idles in their custody, so it is truly free—for them. What if they paid you for online bill-pay?

The power of your capital

These examples sum up to one real-world app and one guy’s back-of-the napkin scribbling, but what innovations can be found if thousands are thinking along these lines? What if new options can be configured, new efficiencies imagined, and solutions programmed and secured for millions who know nothing of programming or finance ? What if capital was as easy to accumulate and use in Mongolia—yes, there is a popular Terra app in Mongolia—as it is in Florida? A ‘normie’ revolution of people taking back control of their own funds maybe?

Just some random thoughts.

Further perspective:

Pantera Capital founder, Terra backer:

https://medium.com/ico-alert/mobile-payments-a-blockchain-utility-ripe-with-opportunity-ce12b7f5980f

Do Kwon interview: